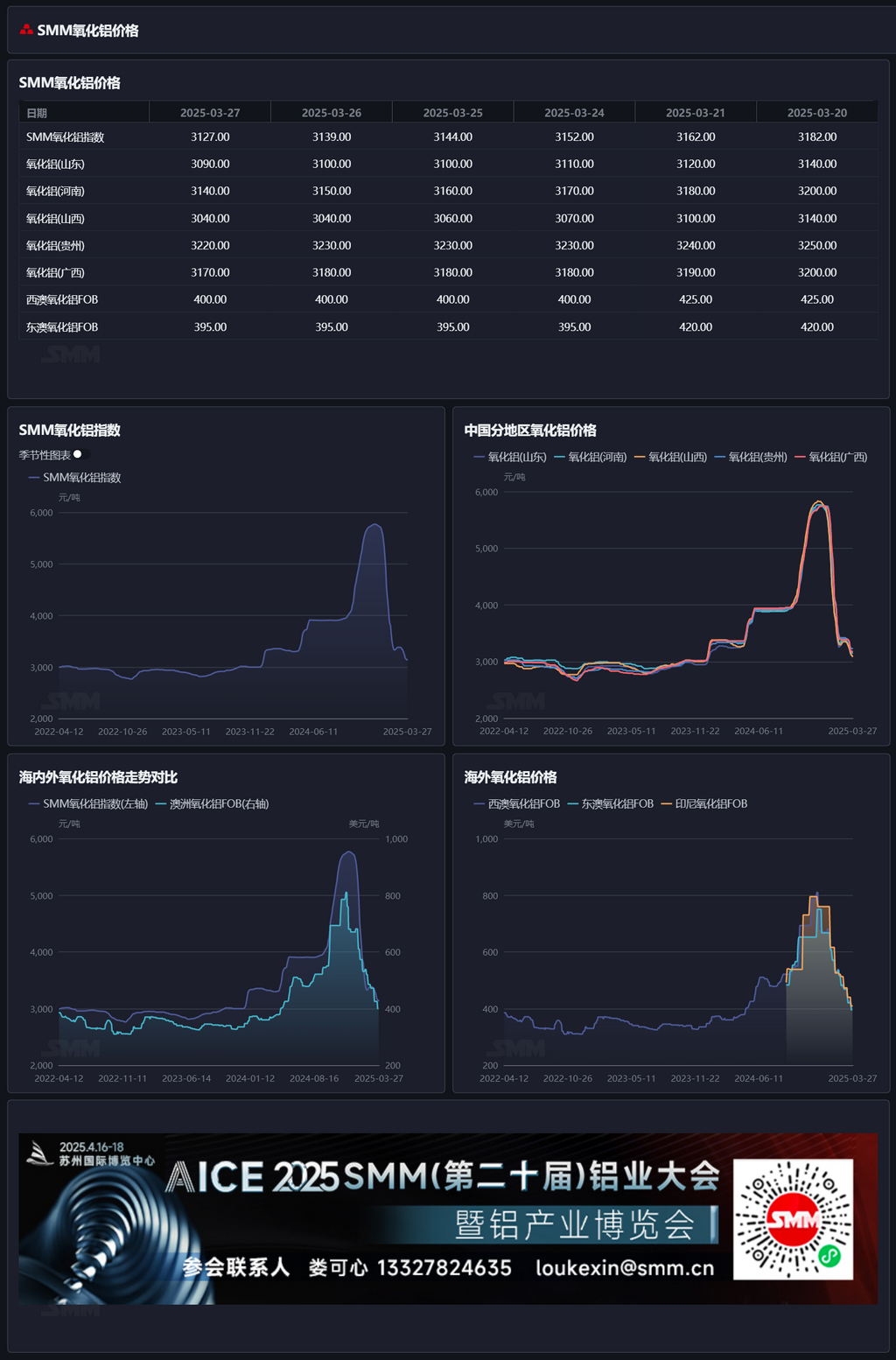

SMM Alumina Morning Comment 4.2

Futures market: In the night session, the most-traded alumina 2505 futures contract opened at 2,946 yuan/mt, with a high of 2,954 yuan/mt, a low of 2,932 yuan/mt, and closed at 2,942 yuan/mt, down 9 yuan/mt or 0.30%, with an open interest of 195,000 lots.

Ore side: As of April 1, the SMM imported bauxite index stood at $93.1/mt, flat from the previous trading day. The SMM Guinea bauxite CIF average was $91/mt, flat from the previous trading day. The SMM Australia low-temperature bauxite CIF average was $87/mt, flat from the previous trading day. The SMM Australia high-temperature bauxite CIF average was $81/mt, flat from the previous trading day.

Industry updates:

- Spot alumina: On Tuesday, it was learned that an aluminum plant in Xinjiang tendered to purchase some alumina, with a transaction price of around 3,270 yuan/mt delivered to Xinjiang.

- On April 1, the exchange issued a notice stating that, after research, it has been decided that starting from the trading session on April 8, 2025 (i.e., the night session on April 7), the trading fee for alumina futures will be adjusted to 0.01% of the transaction amount, and the intra-day closing fee will be adjusted to 0.01% of the transaction amount.

Spot-futures price spread report: According to SMM data, as of 11:30 am on April 1, the SMM alumina index was at a premium of 128 yuan/mt against the most-traded contract's latest transaction price.

Warrant report: On April 1, the total registered volume of alumina warrants increased by 601 mt to 299,100 mt compared to the previous trading day. The total registered volume of alumina warrants in Shandong remained flat at 4,513 mt. The total registered volume of alumina warrants in Henan decreased by 900 mt to 24,900 mt. The total registered volume of alumina warrants in Guangxi remained flat at 49,800 mt. The total registered volume of alumina warrants in Gansu decreased by 903 mt to 21,600 mt. The total registered volume of alumina warrants in Xinjiang increased by 302 mt to 196,700 mt.

Overseas market: As of April 1, 2025, the FOB alumina price in Western Australia was $377/mt, with an ocean freight rate of $21.40/mt. The USD/CNY exchange rate selling price was around 7.29, which translates to a domestic mainstream port selling price of around 3,075 yuan/mt, 285 yuan/mt higher than the domestic alumina price. The alumina import window remained closed. Based on the latest FOB transaction price of $368/mt in Eastern Australia, the domestic mainstream port selling price is estimated to be around 3,300 yuan/mt, less than 200 yuan/mt higher than the SMM alumina price index. If overseas alumina prices further decrease and the rate of decrease exceeds that of domestic prices, the alumina import window may gradually open. On the export side, based on the latest spot alumina transaction price in Shandong, the domestic alumina export cost is estimated to be around $450/mt, higher than the overseas spot alumina price, and the export window remains closed.

Summary: Last week, the weekly operating rate of alumina was lowered again, and the national total operating capacity of metallurgical alumina decreased to 87.3 million mt/year, with the weekly operating capacity down 700,000 mt/year WoW. However, the overall loose supply situation in the alumina market has not yet reversed. According to SMM data, as of last Thursday, the total operating capacity of domestic aluminum was 43.88 million mt/year, which translates to an alumina demand operating capacity of around 84.47 million mt/year. The theoretical demand increased slightly again but remained below the actual operating level. On the supply side, domestic bauxite supply remained low with limited increments. The increase in imported bauxite supply pushed up the total domestic bauxite supply, and the bauxite supply-demand fundamentals may become looser than before. In the short term, bauxite prices are expected to remain under pressure. Meanwhile, downstream aluminum plants reported that alumina procurement is mainly based on long-term contract execution, and some plants that have completed winter stockpiling plan to actively reduce inventory. Last week, according to SMM statistics, alumina raw material inventory at aluminum plants decreased by 44,000 mt WoW. In the short term, alumina circulating supply is expected to remain relatively loose, and alumina prices may continue to operate under pressure. Subsequent attention should be paid to changes in alumina operating capacity.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this to replace independent judgment. Any decisions made by clients are not related to SMM.]